Multi-Venue Expansion

Pride’s medium-term growth strategy: opening a second LGBTQ+ venue in either Fitzroy/Collingwood or Frankston (or both, sequentially) to mitigate single-venue risk, improve unit economics, and extend the brand to underserved communities. Expansion is contingent on capital raise and successful stabilisation of the flagship Footscray venue.

⚠ STRUCTURAL BLOCKER: Capital raise is blocked until Corporate Structure Reform resolves the s 113 breach. Expansion planning can proceed but capital commitment cannot.

Strategic Rationale

Risk mitigation: 100% dependency on a single venue in Footscray is structurally unsustainable. Three geographically diversified venues spread revenue and neighbourhood-specific risk.

Unit economics improvement: Current overhead (CEO, Head of Programming, bookkeeper, marketing) is fixed per venue. Expanding to 2–3 venues allows the same central overhead to serve 2–3x revenue base.

Supplier leverage: Multi-location operation increases negotiating power with beverage distributors, performer networks, and service providers.

Fitzroy/Collingwood: The Proven Market Play

Per LGBTQ Venue Expansion Research (April 2026). Lower-risk, higher-cost.

Market Position

6–8 operating queer venues concentrated on a 600m Smith Street corridor (Sircuit, UBQ/LCKR Room, The 86, Evie’s, Yah Yah’s, The Laird, The Peel, DT’s). Despite this density, the market is not saturated — it is heavily skewed toward gay men, with five material gaps:

- Women’s/AFAB dedicated space (Critical) — Beans Bar (Melbourne’s only dedicated lesbian/trans/NB bar) closed March 2025. No permanent replacement. Community actively seeking this.

- Community-owned venue — every northside venue is commercial for-profit. No community bar model exists. Pride’s structure fills a genuine niche.

- Large-format inclusive late-night (Thu–Sun) — The Peel retreated to Fri–Sat only. No dedicated queer dance club operates Thu–Sun with inclusive programming.

- Dedicated 200+ cap performance room — The 86 operates at ~150 capacity Thu–Sat only. No properly equipped 200–300 seat performance/cabaret room exists.

- Inclusive multi-demographic space — Rainbow House closure (early 2024) left a gap for BIPOC, trans, and AFAB performers.

Costs and Feasibility

| Factor | Range |

|---|---|

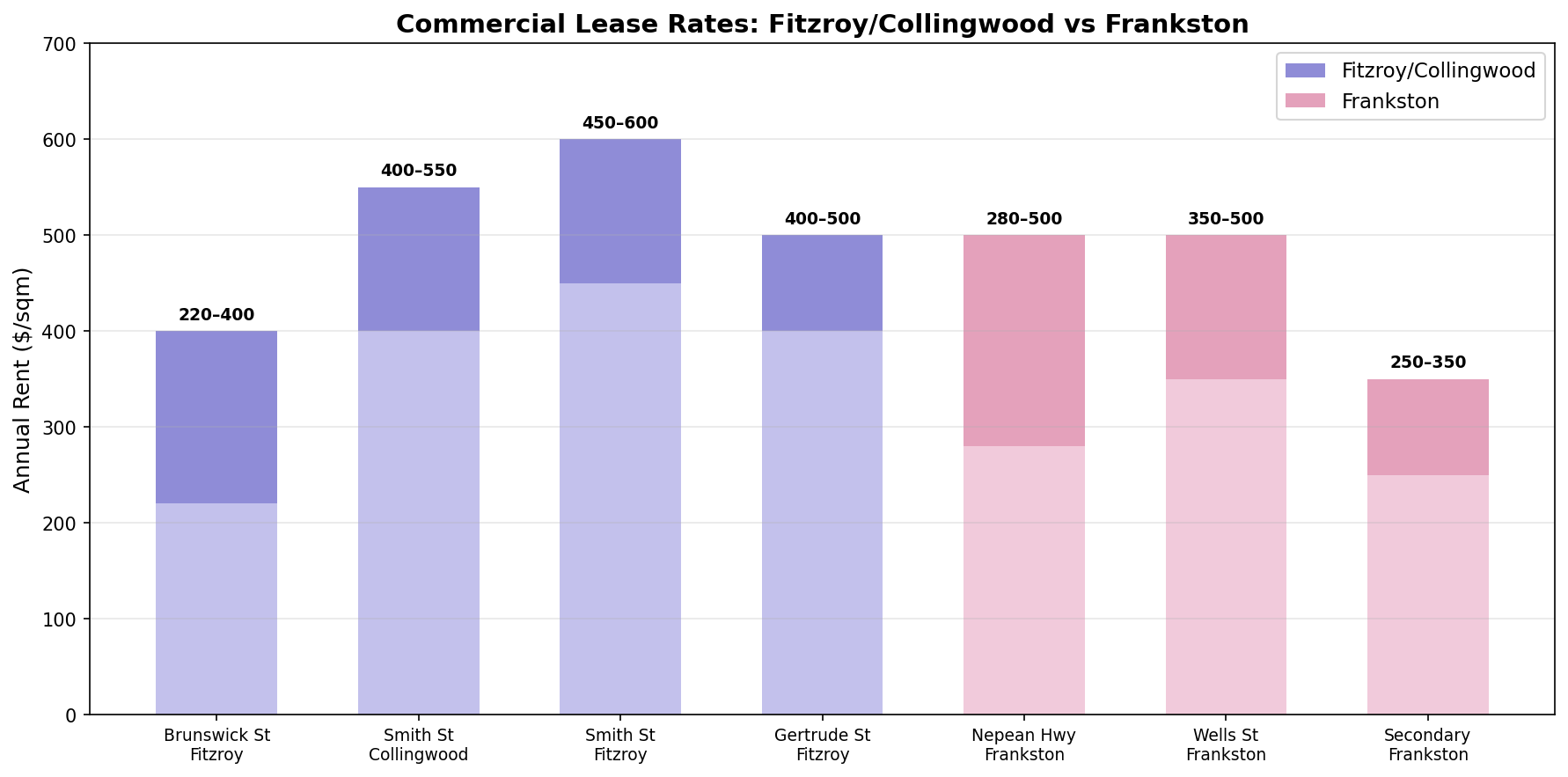

| Lease rate (Smith St) | $400–$600/sqm p.a. |

| Lease rate (Brunswick St — more affordable) | $220–$400/sqm p.a. |

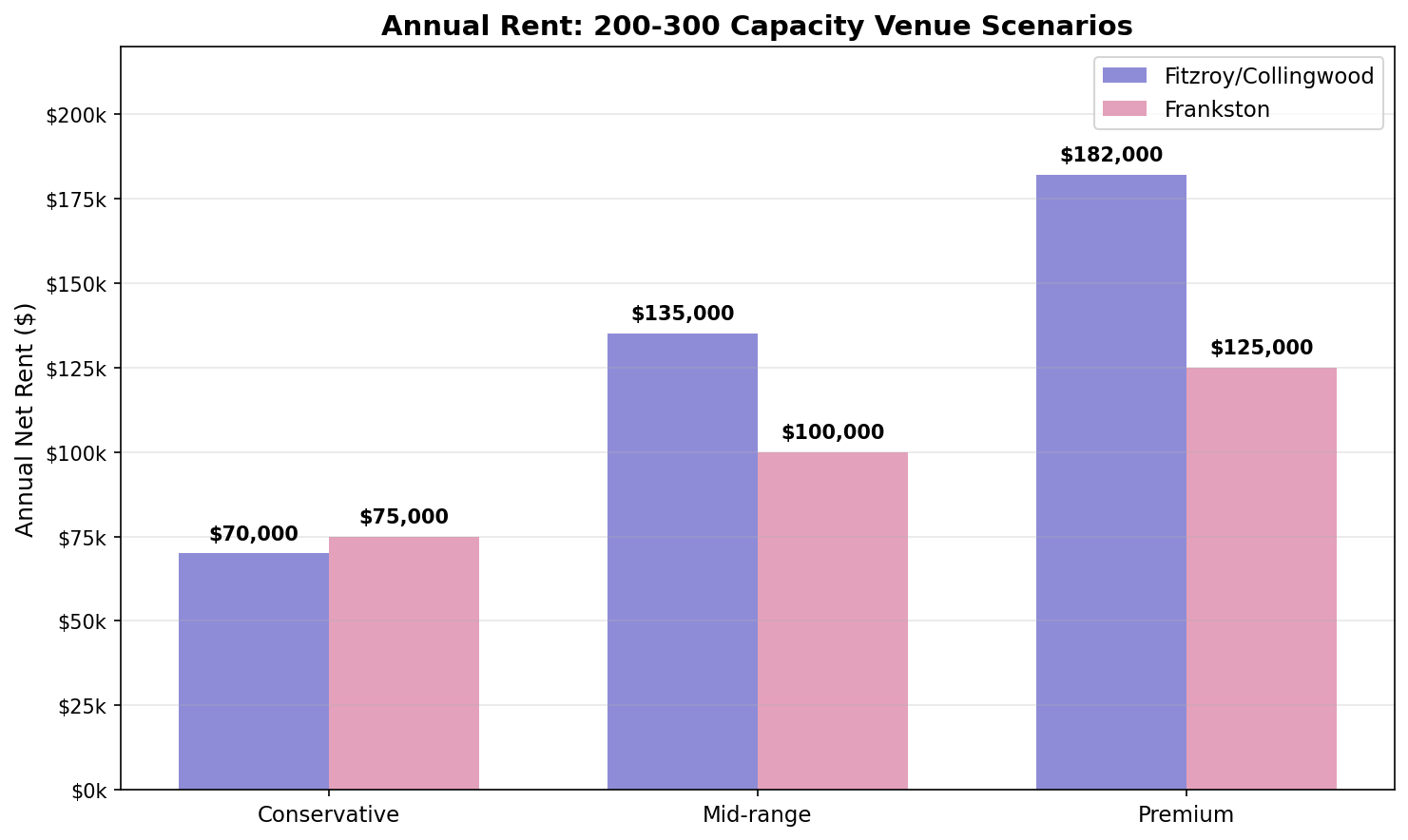

| Annual rent (250 sqm venue) | $100,000–$150,000 (Smith St); $55,000–$100,000 (Brunswick St) |

| Fitout costs | $2,000–$5,000/sqm ($500k–$1.25M for 250 sqm) |

| Late-night licence application | $1,260–$2,269 + 5 supplementary documents (Yarra-specific) |

| Outgoings | 15–25% on top of base rent |

Regulatory Environment

- No late-night licence moratorium (expired June 2015). Yarra has ~280 licensed venues open after 10pm, 90 past 1am.

- Live Music Precincts (Amendment C331yara, December 2025) cover Smith Street — new residential must self-soundproof under Agent of Change provisions.

- LGBTQ+ Heritage Study (May 2025) — Yarra Council granted heritage protection to The Laird, noted Yarra has 5x the state average of same-sex marriages. Signals active council support.

- Five supplementary documents required for Yarra late-night applications: supplementary form, Venue Management Plan, Noise Mitigation Strategy, History of Compliance, Gender-Based Violence Prevention and Response Plan.

Population and Development

Yarra population projected to grow from ~103,700 to 142,000 by 2035 (+37%), with Fitzroy/Collingwood/Abbotsford driving 85% of growth. 25–34 cohort +30%, 35–49 +32% — core nightlife demographic. Fitzroy Gasworks (433 Smith St): ~1,200 new apartments by late 2028, directly adjacent to the queer village strip.

Priority Sites

- 108 Smith Street, Collingwood — former Rainbow House Club, reportedly available, directly on the queer strip

- Brunswick Street — most affordable option if Smith Street proves prohibitive

Recommended Positioning (Fitzroy)

Anchor on women’s/AFAB programming (highest-priority gap), community governance structure (unique value proposition), dedicated 200-cap performance room for diverse booking, and late-night Thursday through Sunday (fills The Peel’s retreat).

Frankston: The Market-Creation Play

Per LGBTQ Venue Expansion Research (April 2026). Higher-risk, lower-cost, absolute white space.

Market Position

No LGBTQ+-identified venue has ever operated in Frankston or anywhere on the Mornington Peninsula. This is a confirmed historical white space — Melbourne’s queer bar history is overwhelmingly inner-city.

Community infrastructure exists: Peninsula Pride (government-funded youth program), Frankston Queers (Instagram-active social group), LGBTIQA+ Collaborative (cross-council body), Mornington Peninsula Queers. Midsumma Festival has run on the Peninsula for four consecutive years (2023–2026).

Late-night hospitality is thin: Pier Hotel/Bandroom (1,200+ cap, dominant operator), Moon Dog Beach Club (2,000 sqm, opened late 2024), but no venue regularly trades past 1am. No dedicated nightclub operates.

Costs and Feasibility

| Factor | Range |

|---|---|

| Vacancy rate | 23% (96 vacant properties, Council audit May 2025) |

| Lease rate (Nepean Hwy fitted) | $400–$500/sqm p.a. |

| Lease rate (secondary CBD) | $250–$350/sqm p.a. |

| Annual rent (250–350 sqm) | $75,000–$133,000 |

| Incentives | Rent-free periods (1–6+ months), landlord fitout contributions likely |

| Council grants | Up to $50,000 (“Eat Street” hospitality stream); $4k–$10k artist grants |

Frankston is 40–60% cheaper than comparable Fitzroy/Collingwood locations. The 300% differential rate on long-term vacant commercial properties (from July 2026) further pressures landlords to fill spaces.

Regulatory Environment

- No late-night licence restrictions. Frankston CBD is not a declared lockout area; no cumulative impact restrictions.

- ACZ1 rezoning (Amendment C160fran, gazetted April 2025) — enables up to 16-storey towers, streamlines approvals, explicitly designates CBD for “leisure and entertainment.”

- VC286 (1 July 2025) — no planning permit required for liquor. Standard state requirements only (no Yarra-style supplementary documents).

- Council is a “Small Business Friendly Council” (Victorian Small Business Commission).

Population and Development

- Catchment: Frankston LGA (~144,615) + Mornington Peninsula (~250,000+) = ~400,000 people with zero LGBTQ+ venue infrastructure

- $506M in private CBD development approved/under construction (770+ apartments)

- $1.1B Peninsula University Hospital opened early 2026 (940+ Monash clinical students annually)

- Frankston Line reconnected to City Loop February 2026

- $50M Nepean Highway Boulevard redevelopment under way

- Est. ~14,000–21,000 LGBTQ+ community in Frankston LGA (based on ~600–650 same-sex couples)

Available Sites

- 433 Nepean Hwy (236 sqm) — ex-restaurant/bar, existing liquor licence for 141 patrons, kitchen + alfresco

- 489 Nepean Hwy (228 sqm) — full kitchen fit-out

Key Risk

Late-night transport is weak — last train ~12am–1am weekends; Uber dependency. Perception/stigma around Frankston is shifting but not resolved. The market must be created, not captured — requires 12–24 month ramp-up.

Coburg/Brunswick (Not Yet Researched)

Emily Rose described this as “close to queer precinct but rougher around the edges” — lower rent than Fitzroy, authentic working-class identity similar to Footscray. Geographic proximity to existing LGBTQ+ community + similar neighbourhood character. Requires dedicated feasibility research comparable to the Fitzroy/Frankston analysis.

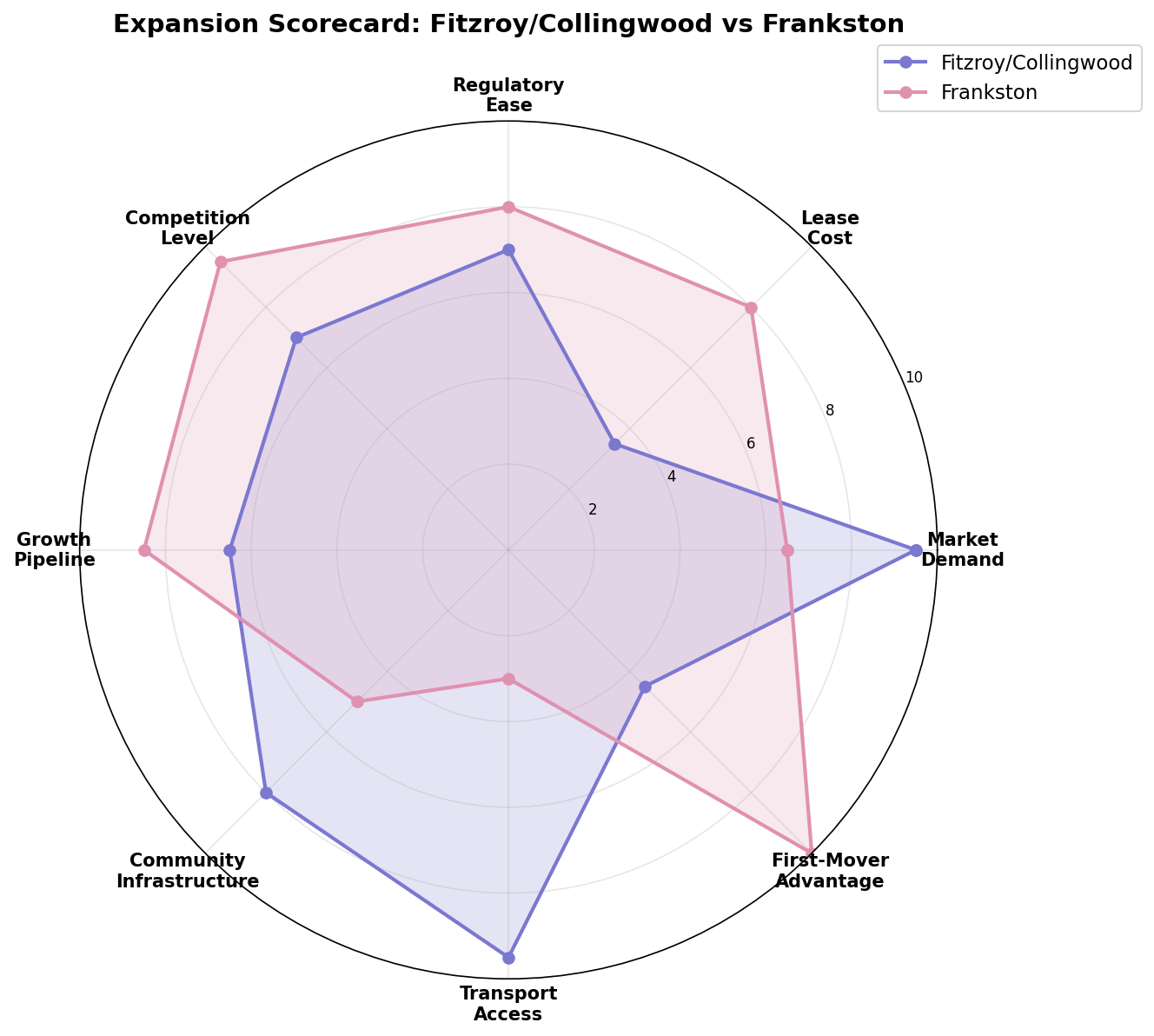

Comparative Summary

| Factor | Fitzroy/Collingwood | Frankston |

|---|---|---|

| Annual rent | $100k–$150k (Smith St) | $75k–$133k |

| Existing LGBTQ+ market | Established (6–8 venues) | None (absolute white space) |

| First-mover advantage | Moderate (fills gaps) | Absolute (regional monopoly) |

| Catchment | ~103k growing to 142k | ~400k (LGA + Peninsula) |

| Council grants | Limited | Up to $50k |

| Late-night transport | Excellent | Weak (last train ~1am) |

| Regulatory complexity | 5 supplementary documents | Standard state requirements |

| Market risk | Low | High (must create from zero) |

| Cost pressure | High | Moderate (40–60% cheaper) |

Not mutually exclusive. Fitzroy is the logical next step for a proven operator. Frankston is the longer-horizon strategic bet. Frankston’s lower cost base means a venue there could survive a slower ramp-up — whereas Fitzroy must trade profitably from day one.

Expansion Readiness

Systems Ready for Multi-Site

- Square POS: multi-location configuration mature

- Xero: centralised accounting with per-location P&L

- Google Workspace: distributed team infrastructure

- TryBooking: multi-venue ticketing supported

- Humphrey Intelligence App: designed for multi-venue analytics

Required Pre-Expansion

- Systems documentation (current workflows are ad hoc)

- Written brand guidelines

- Multi-site reporting dashboards

- Community consultation in target location (see framework below)

Community Consultation Framework

Before committing capital, each location requires: local LGBTQ+ stakeholder engagement, brand positioning test, venue and lease assessment, competitor analysis, and location-specific financial modelling.

Key Facts

- Fitzroy gap analysis identifies 5 material programming gaps despite 6–8 existing queer venues

- Frankston is a confirmed absolute white space — no LGBTQ+ venue has ever operated on the Mornington Peninsula

- Frankston rent is 40–60% below inner-Melbourne equivalents

- Both markets’ regulatory environments are supportive (no licence moratoria)

- Expansion blocked until Corporate Structure Reform resolves s 113 breach and Capital Raise Strategy secures $200k–$400k

Related Pages

- LGBTQ Venue Expansion Research — source research (Apr 2026)

- Strategic Plan — capital raise and expansion rationale

- Capital Raise Strategy — funding mechanics (blocked until structural reform)

- Corporate Structure Reform — structural prerequisite for capital raise

- Brand Positioning — community identity and values framework

- Staffing Model — organisational structure for multi-site operation

- Competitor Landscape — venue analysis including Fitzroy/Collingwood detail

- Grant and Funding Eligibility — Frankston council grants (up to $50k hospitality)